STORIES OF IMPACT

/

Articles by Endurance / A Shrinking Money Supply and Rising Rates Presents Liquidity and Capital Challenges for Banks by Stephen Curry

A Shrinking Money Supply and Rising Rates Presents Liquidity and Capital Challenges for Banks by Stephen Curry

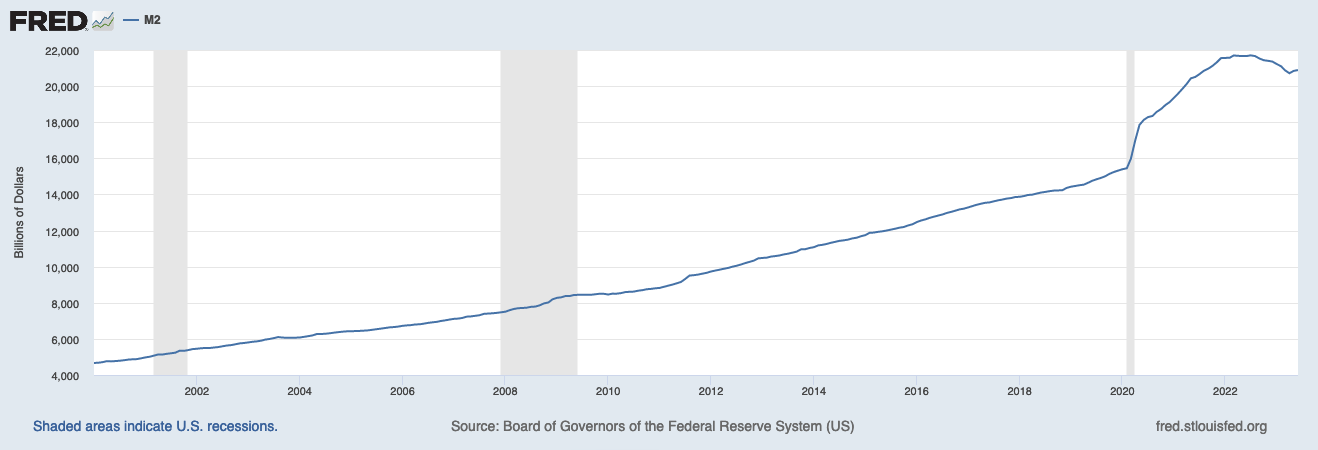

The most common measure of money supply, M2, experienced a dramatic and historic run up in 2020-21. As a result of this influx of funds, and the many dislocations attributable to COVID, reducing the money supply to mute the effects of inflation became a strategic focus of the Federal Reserve in 2022 and 2023. To get back on trendline, the Fed will need to remove additional $2.0-2.5 trillion of M2. Some of this will come through quantitative tightening, some through the Reverse Repurchase Market and some through further rate hikes.

Below is a chart of M2 balances since 2000 from the Federal Reserve.

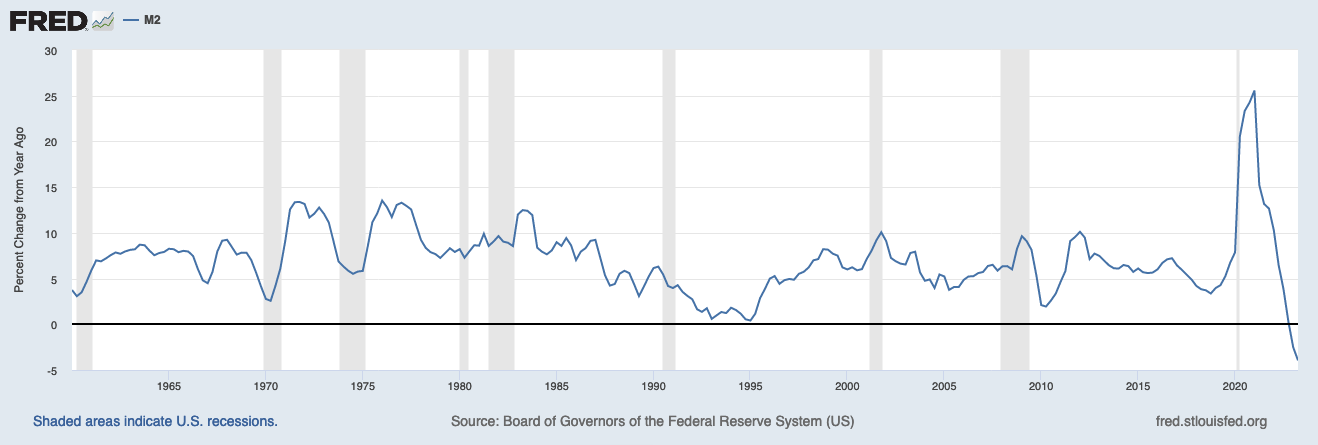

And a chart of the percentage change in M2 since the measure was first established.

A shrinking money supply has significant implications, directly or indirectly, for bank liquidity and the overall financial system, particularly when the moves are substantial. As the money supply contracts, there's less money available in the economy, which affects banks' ability to maintain sufficient liquidity to meet their obligations. Here's how a shrinking money supply can impact bank liquidity:

1. Reduced Deposit Inflows: A shrinking money supply can lead to decreased deposit inflows into banks. As individuals and businesses have less money to save and spend, they may reduce their deposits in banks, and shift their cash to higher yielding money market funds. This will reduce the overall funds available for banks to lend or invest, impacting their ability to generate income.

2. Increased Deposit Withdrawals:With a contracting money supply, economic activity may slow down, at least in certain sectors or regions, leading to increased uncertainty and financial stress. This could prompt depositors to withdraw their funds from smaller banks. This sudden increase in withdrawal requests can strain banks' liquidity positions.

3. Difficulty in Lending: Banks rely on the availability of funds to provide loans to individuals and businesses. A shrinking money supply can lead to decreased lending activity as banks have fewer funds to lend out. This can have a negative impact on economic growth as businesses may find it harder to secure the financing they need to expand. Higher rates may leed to asset price declines which could pressure collateral values, LTV and borrower stability.

4. Interest Rate Pressure: Banks will face pressure to increase interest rates on deposits to attract and retain customers when the money supply is shrinking. Money market accounts have been the clear beneficiary, at the expense of bank deposits. This pattern is driving compression in bank net interest margins as well as losses on the investment securities held for liquidity purposes

Higher interest rates have made borrowing considerably more expensive for both consumers and businesses, likely to be a drag on economic activity and further pressure borrowers. Commercial Real Estate is a good example, as it is facing both falling collateral values and rising rates as lines roll over the next 24 months.

5. Asset Quality and Defaults: A contracting money supply ultimately leads to reduced consumer spending and business investment, which negatively affects borrowers' ability to repay loans. Economic activity has been strong thus far, but continued rate pressure and declines in bank lending could be felt this Fall. This could increase the risk of loan defaults, putting additional strain on banks' balance sheets and liquidity.

6. Market Turmoil: A shrinking money supply and rising rates might precipitate a recession, financial crisis, or bank failures. These events can lead to market turmoil and reduced investor confidence, further impacting banks' access to funding in the financial markets.

7. Risk Aversion: During periods of economic uncertainty and shrinking money supply, banks may become more risk averse. They might be hesitant to engage in lending or investment activities, which could further constrain liquidity in the broader financial system.

Many of these challenges are being felt today. In response, banks need to adjust their strategies to ensure adequate liquidity. This requires increased focus on managing liquidity buffers, and close monitoring of market conditions. It may also involve more conservative lending practices. Regulatory authorities will be pushing banks to maintain elevated levels of liquidity to safeguard against these types of economic scenarios.

In the current market, banks of all sizes are facing outflows of deposits as HNW clients continue to shift funds to larger banks and money market accounts, and corporate treasurers work to diversify banking relationships to fewer, and larger, banks.

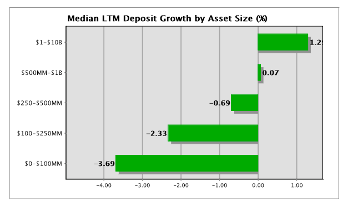

The chart below, sourced from Call Report data provided by QuickRate, displays the shift from deposit growth to contraction in the last 12 months. The quarterly results are much more dramatic.

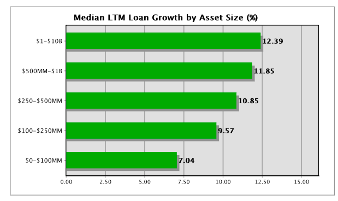

At the same time loan growth has been robust.

Near term balance sheet contraction is underway, particularly at regional banks as they work to improve liquidity while funding deposit outflows. Assets could fall as much as 10-20% in next 3-6 Months. Corresponding cost cuts will follow. Community banks are feeling the cross currents of rising loan demand and falling deposits. Liquidity has been compressed, and many banks are rapidly working to establish liquidity risk management practices, skills which have not been needed by most banks for the last decade.

We see evidence of this distress in the increasing activity under the Fed's BTFP (Bank Term Funding Program), where banks can pledge securities at notional value. Borrowing under this line continues to rise.

The decoupling between bank deposits and money market funds continues to grow.

These changes are magnified by the fractional reserve system used in banking. In a fractional reserve banking system, financial institutions are required to hold only a fraction of their customers' deposits in reserve and can lend out the rest of the deposits. This practice is a fundamental characteristic of modern banking systems, including that of the United States. Fractional reserve banking allows for the creation of money beyond the physical currency issued by the central bank. When banks make loans using their excess reserves, the borrowers typically receive the loan amount in the form of a new deposit. The process of lending out excess reserves and creating new money can have a multiplier effect on the money supply. As the newly created deposits are deposited in other banks, those banks can lend out a portion of those deposits, leading to further increases in the money supply.

While fractional reserve banking enables banks to generate income through lending and investment, it also presents risks. If too many depositors demand withdrawals simultaneously, or if borrowers default on their loans, banks could face liquidity problems or even a financial crisis. To mitigate these risks, regulatory authorities impose capital adequacy requirements and conduct regular stress tests on banks.

This is where we find ourselves today. With a policy to decrease the money supply by the largest amounts since the end of the Second World War and the Great Depression, and sharply rising rates, along with record fiscal deficits, will test the resiliency of many banks, particularly those who benefited the most from low cost deposits the last decade.

This presentation is being furnished on a confidential basis to provide preliminary summary information. The information, tools and material (collectively, information) contained herein is not directed to or intended for distribution or use by any person or entity who is a citizen or resident of or located in any jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Endurance Advisory Partners, LLC, to any registration or licensing requirement within such jurisdiction.

The information presented herein is provided for informational purposes only and is not to be used or considered as an offer to sell, or buy securities or other financial instruments, or any advice or recommendation with respect to such securities or other financial instruments. The information may not be reproduced in whole or in part or otherwise made available without the prior written consent of Endurance Advisory Partners, LLC. Information and opinions presented have been obtained or derived from sources believed to be reliable, but Endurance Advisory Partners, LLC makes no representation as to their accuracy or completeness. Endurance Advisory Partners, LLC, accepts no liability for any loss arising from the use of the information contained herein.

This information is subject to periodic update and revision. Materials should only be considered current as of the date of the initial publication, without regard to the date on which you may access the information. Endurance Advisory Partners, LLC, maintains the right to delete or modify the information without prior notice.

Under no circumstances and under no theory of law, tort, contract, strict liability or otherwise, shall Endurance Advisory Partners, LLC be liable to anyone for any damages resulting from access or use of, or inability to access or use, this information regardless of whether they are dire, indirect, special, incidental, or consequential damages of any character, including damages for trading losses or lost profits, or for any claim or demand by any third party, even if Endurance Advisory Partners, LLC knew or had reason to know of the possibility of such damages, claim or demand.